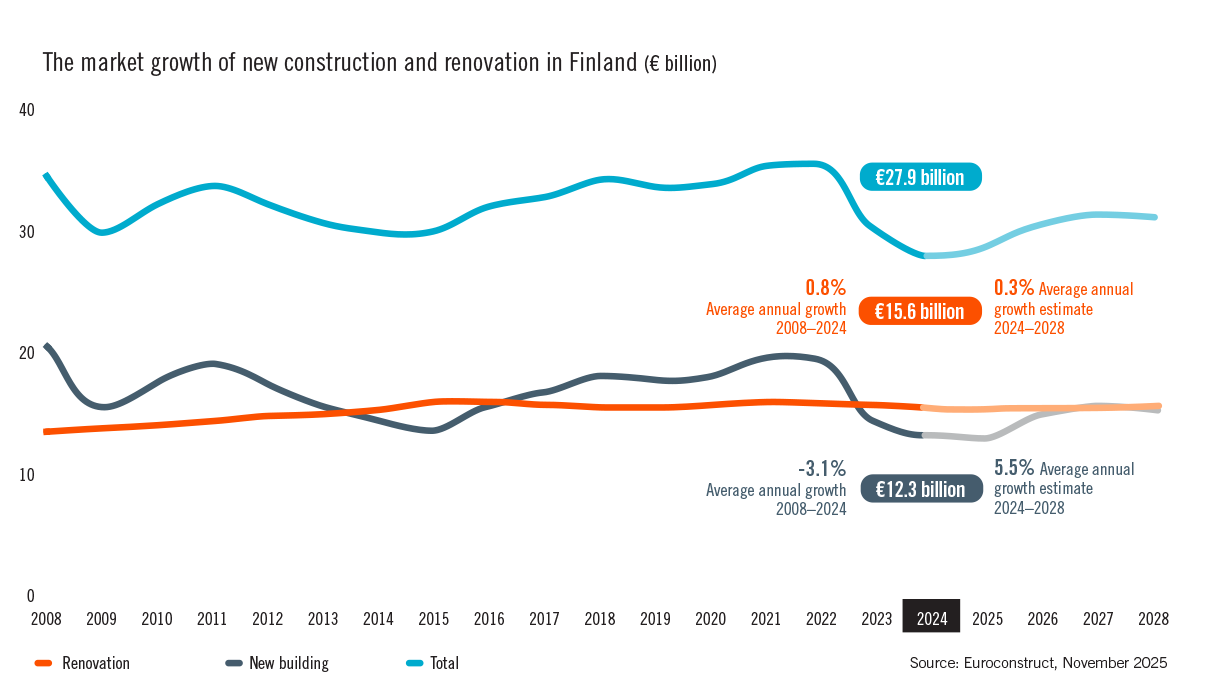

The renovation market

Consti is one of Finland’s leading companies focused on renovation contracting and technical building services. Consti offers comprehensive renovation and building technology services and selected new construction services to housing companies, corporations, investors and the public sector in Finland’s growth centres.

According to the Bank of Finland, the Finnish economy is expected to be moving from a prolonged period of slow growth towards a cautious recovery. However, growth in gross domestic product (GDP) in 2025 is forecast to remain modest. The Bank of Finland estimates that GDP grew by 0.2 per cent in 2025, while growth of 0.8 per cent is expected in 2026.

The deceleration of inflation and the decline in interest rates are gradually supporting the recovery of consumers’ purchasing power and companies’ willingness to invest. Nevertheless, the Bank of Finland estimates that the outlook for the Finnish economy continues to be overshadowed by uncertainties related to international politics and global trade, as well as by the public sector deficit. Weak employment situation and economic uncertainty have decreased private consumption. As real earnings of employees increase and labour market recovers, consumption is expected to pick up in the coming years. The Bank of Finland estimates that non-residential investments declined slightly in 2025 but expects investments to return to growth in 2026.

With the gradual economic recovery, the overall construction market is also expected to begin recovering. However, the return to a growth trajectory has been slower than anticipated. According to the Confederation of Finnish Construction Industries RT, construction output is estimated to have increased by approximately 0.8 per cent in 2025 compared to the previous year, while the market research institute Euroconstruct estimates growth of 3.0 per cent. In 2026, construction is expected to turn towards growth from a low baseline. Construction growth is supported in particular by investments related to the energy transition and data centres. Industrial construction is forecast to increase, due to factors such as government-backed green investments. Investments linked to the defence sector are also driving growth in the construction market. For 2026, RT forecasts growth of 3.5 per cent in construction, while Euroconstruct expects growth of 4.8 per cent.

Growth in new construction has been driven by industrial construction, schools and commercial premises. Industrial construction has been boosted, in particular, by investments in the battery and energy industries. Euroconstruct estimates that non-residential construction increased by 11.1 per cent in 2025 and will grow 10.7 per cent in 2026. RT estimates that non-residential construction declined by 2.0 per cent in 2025 and will increase by 3.0 per cent in 2026.

The market for new residential construction has suffered from a pronounced downturn over several years. Following an exceptionally high level of residential development, housing construction contracted sharply in 2023–2024, declining by approximately 30 per cent per year. In 2025, the number of housing starts remained below the long-term average. According to Euroconstruct, a recovery in residential construction would require an improvement in the housing market, along with increased investor demand and stronger consumer confidence. Residential construction volumes increased by 1.0 per cent in 2025 according to RT and by 2.1 per cent according to Euroconstruct. For 2026, RT forecasts growth of 12 per cent and Euroconstruct 15.7 per cent from low baselines.

Both the Confederation of Finnish Construction Industries RT and Euroconstruct estimate that renovation construction declined by 0.5 per cent in 2025. If the estimates are realised, this would mark the third consecutive year of contraction in the renovation market.

Low levels of new housing starts and the contraction of the renovation market have sustained the intense competition for both renovation projects and building technology contracts.

Euroconstruct estimates that residential renovation returned to modest growth already in 2025. However, renovation projects undertaken by housing companies have been slowed by limited access to financing. Professional renovation is estimated to account for over half of residential renovation, and its proportion has been increasing.Non-residential renovation, particularly in privately owned commercial premises, remained low. Although there is a clear need for renovations and modifications, many projects have been postponed for as much as several years. Contributing factors include rising costs, oversupply of premises, and the low volume of property transactions and related development projects. In particular, there is an increasing need for building purpose modifications due to changes in working methods and the retail sector. Many older premises also no longer meet modern requirements for user comfort.

Public sector renovation investments are expected to remain at a good level. In 2025, renovations of public facilities were particularly concentrated in the education and healthcare sectors. However, the weak financial position of municipalities and wellbeing services counties may constrain renovation activity in the coming years.

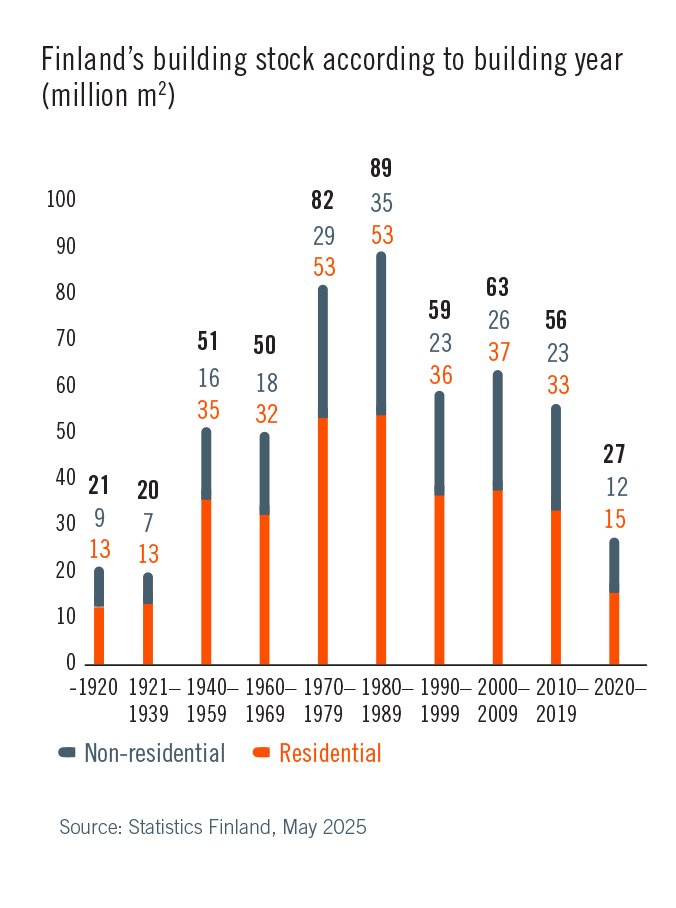

The ageing building stock, urbanisation, changes in space utilisation, and the growing importance of sustainability and the green transition are generating demand and providing a foundation for Consti’s long-term growth.

In renovation construction, demand is largely needs-driven. The need for renovation is increasing not only due to the age of buildings and repairs required as a result of climate change, but also due to societal changes such as population ageing, new requirements for space utilisation, and higher expectations regarding user comfort. Through building purpose modification projects, former office and industrial premises can, for example, be transformed into hotels or residential buildings with accessibility taken into account. In the commercial property market in particular, the EU Energy Efficiency Directive, which entered into force in 2024, and the environmental certification requirements imposed on properties are increasingly evident. Renovation construction plays a key role in reducing the carbon footprint of the built environment, as the volume of new construction increases by only around one per cent annually.

Urbanisation and the concentration of immigration in major cities mean that both new construction and renovation activity are increasingly focused on growth centres.